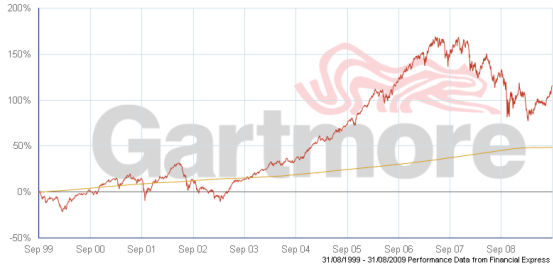

In this graph we see the very best UK cash returns (GLG Institutional Cash Fund) measured against a well known stocks and shares fund (Invesco Perpetual High Income Fund).

The cash fund demonstrates the smooth, straight-lined returns, and the stocks and shares fund represents the spiky volatile returns.

It is simple to see, however, that over a 10-year period the better place to be was stocks and shares – even with significant market volatility over recent years the stocks and shares still offered double the return of cash in the long run, but there would have been some scary moments along the way!

With this in mind, when it comes to finding a home for the Child Trust Fund (CTF) voucher of £250, and potentially up to an additional £100 per month (£1,200 per annum), it is important to consider which approach offers the best long term growth for your child’s CTF.

One thing that cash investing ensures is that whatever the amount invested, on the child’s 18 th birthday, it will not have dropped in value.

The stocks and shares approach comes coupled with investment risk. If the above graph is anything to go by, the child would have done well to move away from stocks and shares in 2007 and into cash at that point – naturally, hindsight comes coupled with 20-20 vision! It is fair to say, however, that over a 10-year period, in spite of significant down-turns, stocks and shares have delivered greater returns than cash over that period.

The stock market is likely to return to its upward trend and offers growth potential. However, we cannot ignore the conundrum – the market has been very volatile recently, and has demonstrated the downside risk dangers, but this means that when it bounces back, if it bounces back, there are significant gains to be made. So, should you invest in shares or cash? Certainly if inflation is a consideration we can ill afford to invest in cash.

There are hundreds of CTF providers, and three generic options – cash, life-styled investment, and stocks and shares investment. The option that will make the most for your child may be a difficult decision to make, and it is prudent to seek independent financial advice before doing so.

An adviser will also be able to help you understand whether you can afford to contribute on top of the government contribution, and there may be other financial matters that you have that could benefit from the overview of a professional. With a new addition to the family affordability is often at full stretch. However, one income may drop away, whilst childcare; kit for the new baby such as push chairs, nursery furniture etc; and life assurance to cover the dependency of the child may also be needed at this stage.

Finally, it is important to remember when making decisions on investing that past performance of investments is not necessarily a guide to future performance, and that the value of investment funds can fall as well as rise.

If you would like to know more about this article please contact Christopher Hunter of AFH Wealth Management Ltd atchristopher.hunter@afhgroup.com ; Tel: 01527 577775 or 07814 195616.

The article above is generic information only and should not be deemed as advice. Please contact us for further information.